AI Document Tools for Surplus Lines Brokers: Which Actually Work

AI DOCUMENT DRAFTING AND REVIEW TOOLS FOR E&S SURPLUS LINES BROKERS: WHAT FITS, WHAT FAILS, AND WHY THE GENERIC ADVICE GETS IT WRONG

You're spending thousands of hours per year on documents that regulators require but that tie up your brokers' time and create liability exposure you may not even have coverage for. This report walks through exactly which AI tools can actually help you in an E&S surplus lines operation — and which ones will create more problems than they solve.

Where Your Money's Actually Leaking

Your uninsurability documentation is the biggest time sink. These are state-specific statutory documents that your brokers are drafting manually, reviewing manually, and signing off on manually — even though they follow predictable patterns. A typical E&S broker team spends 8-12 hours per week on uninsurability letters alone. At fully-loaded labor costs, that's $3,000 to $5,000 per month just sitting in document drafting. And that doesn't count the submission formatting work, the pitch decks for underwriters, the amendment language that has to match prior negotiated terms, or the rising E&O premiums you're paying because carriers are now explicitly asking whether you're using AI tools and how.

The secondary leaks are submission formatting and market prep work. Your team reformats the same data into three or four different underwriter submission templates per placement. That's another 4-6 hours per placement across your operation. But the hidden leak is liability: if an AI tool drafts language that misses a state-specific compliance requirement, or loses the context of what was negotiated in a prior amendment, you own that error. Your signature is on it. Your E&O policy may not cover it.

The Tools That Actually Fit E&S Surplus Lines Insurance Brokers

Generic tools like ChatGPT, Claude, and Microsoft Copilot fail at regulatory documents because they have no training on surplus lines statutes, no understanding of state-specific compliance language, and no audit trail. Use them for brainstorming or internal analysis, but do not use them for uninsurability documentation or any compliance-critical document.

Spellbook and Archipelago are purpose-built for specialty insurance work. Spellbook is strongest on front-end work: submission formatting, pitch decks, and standardized language where the context doesn't shift between documents. Archipelago is designed specifically for specialty broker workflows and complex risk data placement. Both have documented governance and audit trails that your E&O carrier will actually recognize. Definely exists in this space but lacks the hard audit trail evidence that carriers are now demanding.

Here's the conditional logic: If you're handling uninsurability documentation or compliance-critical language, do not use generic tools. If you need submission formatting and underwriter pitch decks, Spellbook with a documented review protocol can help. If you handle complex specialty placements and risk data, Archipelago is worth investigating. And if you use any AI tool for documents that touch compliance or liability, you need written confirmation from your E&O carrier that you have coverage before you implement anything.

The implementation sequence, the specific compliance traps you'll face in E&S surplus lines operations, and the detailed risk matrix for each tool across your actual workflows are in the full report.

- Every tool named and evaluated — ChatGPT, Claude, Microsoft Copilot, Spellbook, Definely

- Which tools fit E&S Surplus Lines Insurance Brokers specifically and which quietly fail

- The compliance traps and implementation risks specific to your slice

- A sequenced recommendation — what to buy first, what to wait on, what to avoid

- Confidence ratings on every finding so you know what's solid

Delivered as a PDF immediately after purchase. No subscription. No upsell.

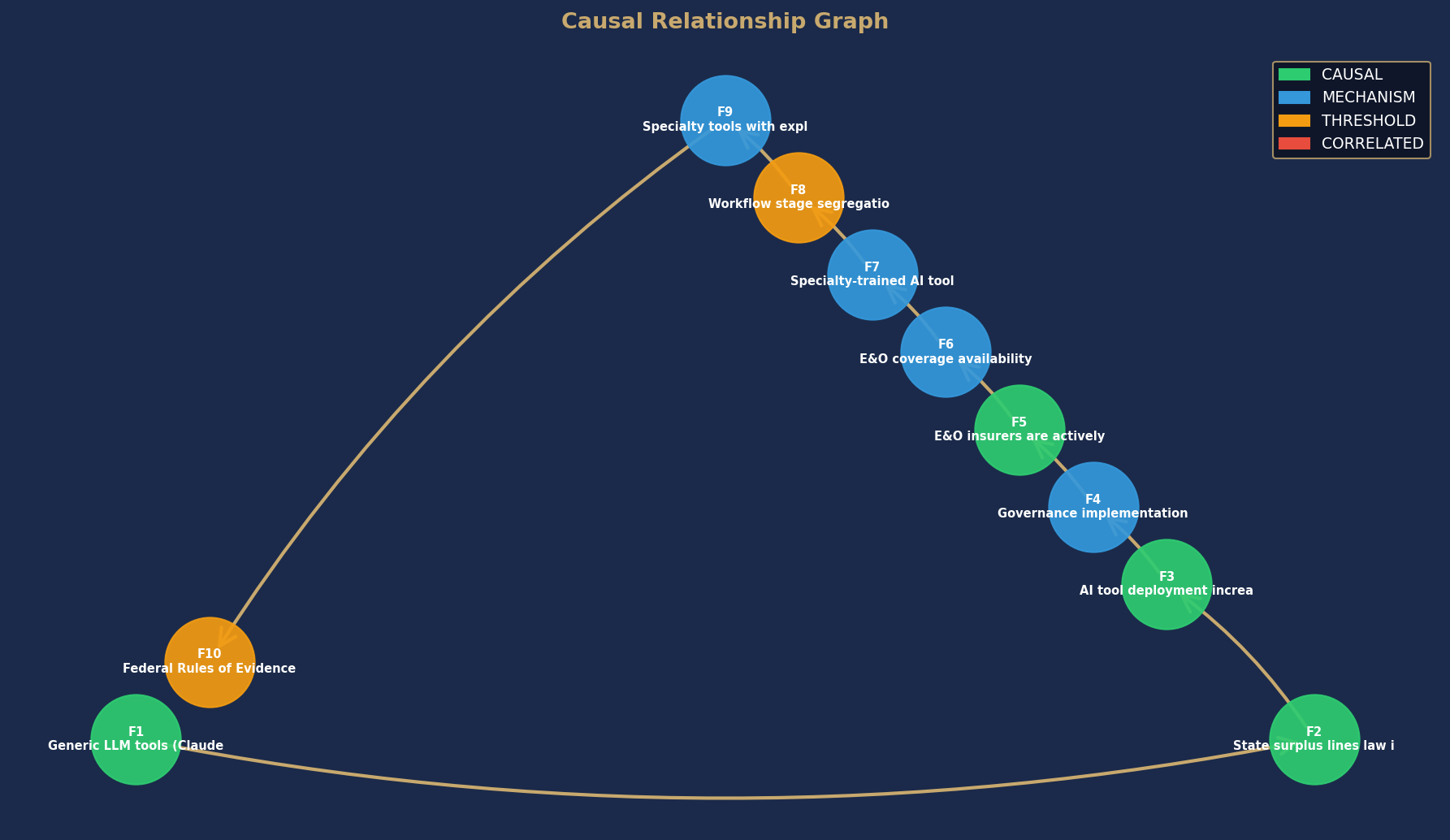

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

- Every AI tool named and evaluated — not placeholders, actual product names

- Which tools fit Independent Insurance Agencies specifically and which ones quietly fail

- The compliance traps and implementation risks specific to your practice area

- Conditional recommendations — which tool fits your specific operation and why

- Confidence ratings on every finding so you know what's solid and what needs validation

Delivered as a PDF immediately after purchase. No subscription. No upsell.

Full report PDF emailed to you immediately after purchase.