HORMUZ INSURANCE DYSFUNCTION: MARKET MECHANISM OR MARKET MIRROR?

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

HORMUZ INSURANCE DYSFUNCTION: MARKET MECHANISM OR MARKET MIRROR?

Executive Summary

The dominant narrative surrounding the 2026 Strait of Hormuz crisis assigns insurance market dysfunction a starring role: premiums exploded, P&I clubs walked away, and the insurance market became the primary bottleneck on global oil flows. That narrative is partially correct and substantially overstated. This report finds that insurance market dysfunction is a real, measurable, and persistent amplifier of trade flow disruption — but the evidence does not support classifying it as the primary independent constraint, and the claim that insurer decisions are leading indicators decoupled from geopolitical events requires significant qualification.

The non-obvious finding is this: insurance market decisions are lagging responses to military risk, not independent constraints that precede or outlast it in a causally meaningful way. When US and Israeli strikes hit Iran on February 28, 2026, insurance premiums spiked within 24 to 48 hours and P&I clubs issued 72-hour cancellation notices on March 1. That sequence looks like insurance driving the disruption. It is actually insurance responding to disruption — and doing so in a way that amplifies and extends it, but cannot be separated cleanly from the military event that triggered both.

The practical implication is important but more modest than the thesis claims. Insurance market signals are useful as persistent indicators of risk that outlast diplomatic announcements. A ceasefire, sanctions relief, or diplomatic framework will not automatically restore underwriting appetite on any predictable timeline. Historical precedent from the 2015 Iran sanctions relief and post-2014 Ukraine periods suggests coverage restoration lags diplomatic resolution by twelve to thirty-six months. That lag is real and consequential for supply chain planning — but the mechanism driving it is institutional inertia and unresolved loss-adjustment cycles, not a clean causal process that operates independently of whether the underlying military risk has actually abated.

Key findings by confidence level:

MECHANISM — War risk premium escalation (0.3 percent to 1.0 to 3.0 percent of hull value) suppresses Hormuz transits through economic cost pressure, but the premium increase cannot be disaggregated from simultaneous military risk as the binding constraint on transit decisions.

MECHANISM — P&I club coverage withdrawal across all twelve International Group members on March 1 functions as an institutional amplifier of disruption, but the withdrawal was responsive to military escalation within 48 hours, not an independent actuarial signal that preceded the crisis.

THRESHOLD — Coverage restoration will likely lag any diplomatic breakthrough by twelve to thirty-six months, based on historical precedents, but the mechanism driving that lag — whether it is loss-adjustment cycles, reinsurance treaty constraints, or continued underlying risk — is not fully specified.

THRESHOLD — Supply chain financing (letters of credit, trade credit insurance) faces secondary pressure from insurance market dysfunction, but direct evidence of L/C rejection rates for Hormuz-route cargoes in May 2026 is absent from available data.

CORRELATED — Traffic volume collapse from 138 vessels per day to five to six vessels per day correlates with insurance withdrawal but cannot be attributed to it, given the simultaneous military blockade.

The practical takeaway for supply chain operators and investors: do not assume a ceasefire restores normal logistics. Do track P&I underwriting circulars and reinsurance treaty renewals as durable signals of whether commercial normalcy is returning. Do not treat current insurance premiums as a primary cause of disruption — treat them as a persistent symptom that will require its own resolution timeline independent of whatever the diplomats announce.

Situation and Context

On February 28, 2026, the United States and Israel launched coordinated air strikes on Iran, triggering what has become the 2026 Strait of Hormuz crisis. [18] Iran retaliated by effectively closing the Strait to commercial traffic, reducing vessel transits from a historical average of approximately 138 vessels per day to five to six transits per day by early May. [9] The Strait carries roughly 25 percent of the world's seaborne oil trade and 20 percent of global liquefied natural gas shipments, making this closure the most significant chokepoint disruption in modern maritime history. [18]

The insurance market responded with extraordinary speed. Within 24 to 48 hours of the strikes, war risk premiums for Gulf tanker movements spiked from a pre-war baseline of approximately 0.3 percent of hull and machinery value to between 1.5 and 3.0 percent — a five- to ten-fold increase. [3] [4] By March 30, premiums had eased to approximately 1.0 percent but remained three to eight times pre-war levels. [21] For a vessel with a hull value of 100 million dollars, a 1.0 percent war risk premium translates to a one million dollar additional insurance cost per transit — before accounting for rerouting expenses.

The P&I club response was more structurally significant. All twelve members of the International Group of P&I Clubs, which collectively insure approximately 90 percent of the world's ocean-going tonnage, issued formal 72-hour notices of cancellation for war risk covers tied to Iran and adjacent Gulf waters, effective March 1, 2026. [10] [15] Specific clubs — including NorthStandard, the London P&I Club, and the American Club — suspended war risk insurance for vessels in Iranian waters and the broader Persian Gulf. [49] This was not a price signal; it was a coverage availability decision.

The London Market Association subsequently clarified that coverage remained technically available for the region, though at elevated premiums, and that 88 percent of Lloyd's marine war market participants retained underwriting appetite for hull war risks. [1] [16] This created a visible bifurcation: hull war coverage remained available through Lloyd's syndicates on a per-placement basis; P&I war risk coverage for Iranian-adjacent routes was effectively withdrawn through club cancellations. [52] [53]

Shipping carriers responded with emergency war risk surcharges and widespread rerouting via the Cape of Good Hope. [15] [37] As of April 2026, rerouting vessels around Africa, combined with insurance cost escalation, had pushed shipping costs up more than 20 percent on key global routes. [26] The rerouting adds approximately two weeks of transit time and materially increases fuel consumption, compounding the insurance-driven cost burden.

Iran's response included a reported plan to offer its own insurance coverage for vessels transiting under Iranian clearance, with few foreign commercial ships visibly transiting as of mid-May 2026. [39] The US Development Finance Corporation was reportedly being considered as a backstop insurer for vessels in the Persian Gulf, signaling that government intervention in the insurance market was being contemplated to compensate for private market withdrawal. [57] The World Economic Forum noted that governments were increasingly being forced into the role of insurer of last resort. [19]

The crisis sits against a backdrop of pre-existing market stress. The Red Sea disruption of 2023 to 2025 had already elevated war risk premiums for a major alternative route. [30] Marine war insurance renewal cycles were already experiencing capacity constraints heading into 2026. [31] The Hormuz crisis therefore hit a market that had not fully recovered from prior chokepoint disruptions, accelerating dynamics that were already underway.

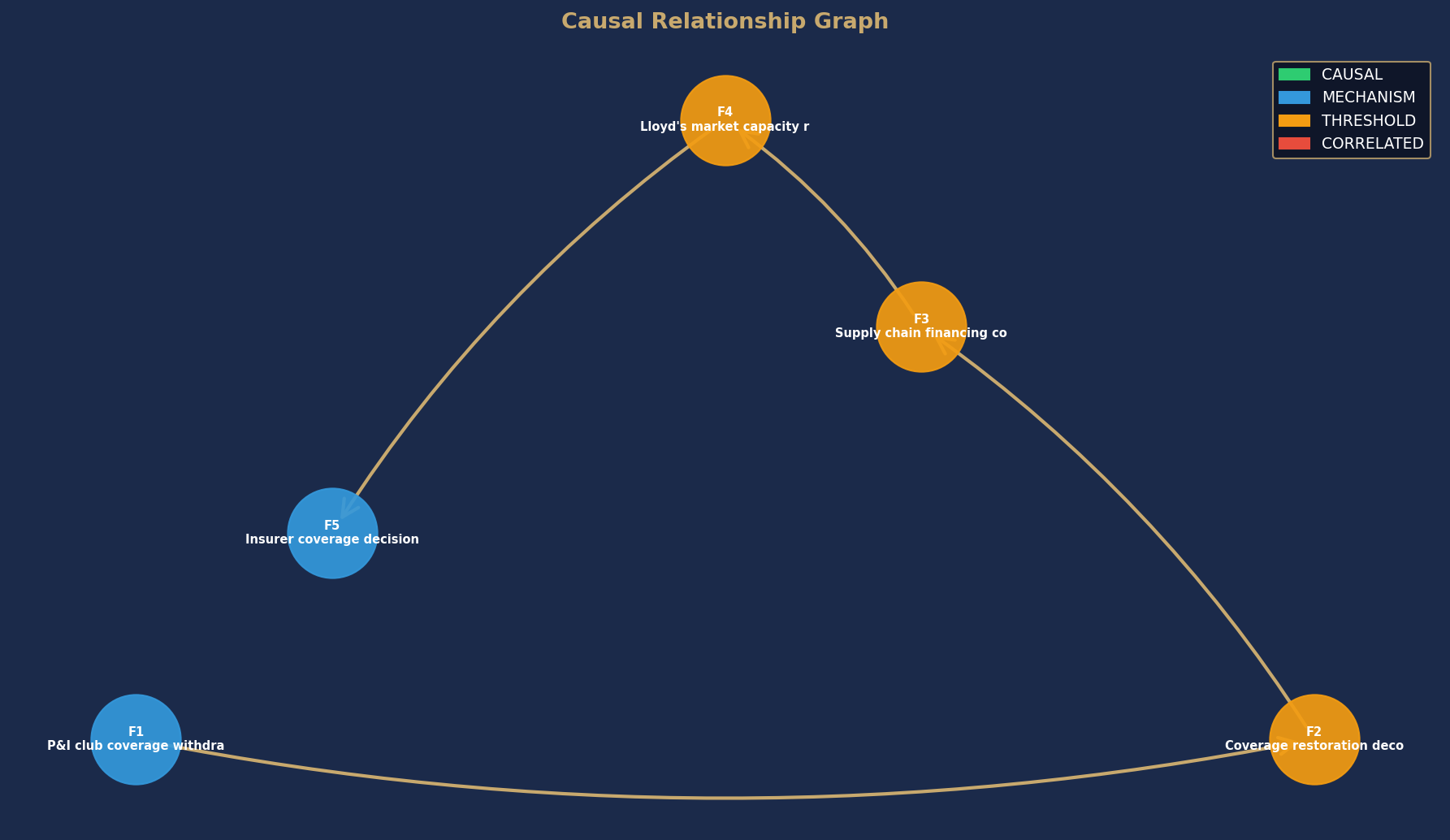

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Causal Analysis, Who Benefits and Why, Key Risks, and What to Watch are available in the full report.

Get the full analysis.

The full report includes the complete causal analysis with confidence ratings, differentiated beneficiary assessment, key risks, and specific data points to watch. Delivered as a PDF immediately after purchase.