S-1 INFORMATION ASYMMETRY AND PRE-DISCLOSURE MARKET DYNAMICS: WHAT THE EVIDENCE ACTUALLY SUPPORTS

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

S-1 INFORMATION ASYMMETRY AND PRE-DISCLOSURE MARKET DYNAMICS: WHAT THE EVIDENCE ACTUALLY SUPPORTS

Executive Summary

The non-obvious finding in this analysis is not that information asymmetry exists in the S-1 filing process — it does, and the evidence for that is solid. The non-obvious finding is that the two most practically interesting questions embedded in this topic — whether asymmetry creates exploitable positioning opportunities today, and which institutional positions already reflect non-public knowledge — are both unanswerable from available public data, and answering them confidently would require either investigative access that regulators possess or the commission of securities fraud.

This distinction matters because the framing of the topic implies a straightforward intelligence problem: detect the asymmetry, map the beneficiaries, and position accordingly. The analytical record shows this framing is wrong at every stage. The asymmetry is real. The mechanisms are partially described. The attribution is impossible, and the "exploitation" question is legally toxic.

What the evidence does support, at CAUSAL confidence, is narrow but important. First, S-1 information asymmetry has historically generated exploitable profits for actors with gatekeeper access — this is proven retrospectively by federal enforcement actions, including the May 2026 SEC case charging 21 individuals and a separate consultant prosecution generating documented gains of over $489,000. [1][5] Second, the regulatory framework governing quiet periods, confidential submissions, and underwriter conduct was constructed precisely because this asymmetry creates material market distortion — the existence of the rules is evidence of the recognized problem, though not proof of deterrent effectiveness. [32][50] Third, trading on material non-public information obtained through S-1 access is a prosecuted federal crime, full stop. [1][5][6]

What the evidence supports at MECHANISM confidence, with important caveats, is that multiple leakage pathways exist — through related-entity regulatory disclosures, counterparty credit repositioning, and option market microstructure — and that these pathways are directionally plausible. However, none of them have been empirically validated in real-time prospective detection. The web search record explicitly confirms that no current data exists on institutional trading pattern anomalies in correlated assets during the 30-90 day pre-announcement window. [Education source 7 query response]

The most important analytical conclusion is this: the framing of "exploitable positioning opportunities" is the wrong frame. The correct frame is regulatory and structural risk. For compliance officers, risk managers, legal counsel, and regulators, the mechanisms described here represent live exposure channels that enforcement agencies are actively targeting. For market participants without MNPI access, the option microstructure and correlation divergence signals described theoretically are not validated detection tools — they are theoretical frameworks awaiting empirical testing that has not been done.

This report proceeds on that basis. It does not identify specific institutional positions, name specific current pre-filing companies, or provide operational guidance for trading on inferred information asymmetry. It does explain why the asymmetry is real, where the leakage channels are, who structurally benefits, and what the enforcement and regulatory environment looks like in May 2026.

Situation and Context

The S-1 registration process creates a structured, legally mandated information asymmetry that persists for a measurable window before public disclosure. Under current SEC rules, companies may submit draft S-1 registration statements confidentially under Rule 418 and the JOBS Act framework, with the SEC permitting review before public filing. [32] Companies are not required to make these filings public until 15 days before the roadshow. During this window — which can extend months — a defined universe of actors possesses information that the broader market does not: the issuing company's executives and board, its underwriting syndicate, legal counsel, auditors, and select institutional investors in pre-marketing conversations.

This population is not small. A typical mid-to-large IPO involves two to three lead underwriters, each with teams of investment bankers, legal advisors, equity research analysts, and sales traders. Legal counsel for the issuer and underwriters may involve dozens of attorneys across multiple firms. Audit teams at Big Four firms include engagement partners, managers, and staff. Pre-marketing conversations with institutional anchor investors, while carefully structured under Regulation FD and Securities Act gun-jumping rules, nonetheless introduce additional parties into the information perimeter. [27][49]

The regulatory framework attempts to manage this asymmetry through several mechanisms. Quiet period rules restrict public communications from company management and underwriters. [49][53] The Volcker Rule and its implementing regulations restrict proprietary trading by banking entities affiliated with underwriters, with information barriers ("Chinese walls") required between banking and trading divisions. [50][54] Section 16 of the Securities Exchange Act requires officers, directors, and 10-percent shareholders to report transactions within two business days. And Rule 10b-5 prohibits trading on material non-public information regardless of how it was obtained.

Despite this infrastructure, enforcement actions in 2026 confirm that MNPI-informed trading continues to occur. The SEC's Division of Enforcement charged 21 individuals in what it described as a wide-reaching insider trading scheme, seeking injunctive relief, disgorgement, and civil penalties. [5] A separate action prosecuted a consultant who traded on confidential clinical trial results obtained through a consulting engagement, generating over $489,000 in documented gains. [6] The SEC's 2026 enforcement priorities explicitly identify insider trading and market manipulation as primary targets, with the Market Abuse Unit deploying advanced data analytics. [1][6][37]

The current IPO environment in 2026 adds practical significance to this analysis. After a subdued 2022-2023 window and a partial recovery in 2024-2025, the IPO pipeline entering 2026 carries significant pent-up inventory of pre-filing companies, including candidates at very large valuations — reports cite IPO-ready companies potentially carrying equity valuations in the range of $100 billion. [20][22] Private equity and venture capital portfolios contain large backlogs of portfolio companies approaching listing readiness, with secondary market activity in pre-IPO shares accelerating as investors seek liquidity ahead of public markets. [23][24] This environment maximizes the number of confidential pre-filing windows open at any given time, correspondingly maximizing the population with MNPI access and the magnitude of the information advantage.

Institutional trading patterns have shifted structurally in the current market. The retail-to-institutional transition documented in 2025-2026 — spot Bitcoin ETF inflows, continued equity market participation, and the institutionalization of digital asset allocation — means that institutional actors now dominate market microstructure in ways that make pre-announcement positioning both more impactful and, potentially, more detectable. [10][12][15]

The tension between these forces — an active IPO pipeline, a growing institutional investor base, documented MNPI exploitation, and sharpened enforcement — defines the current information asymmetry landscape.

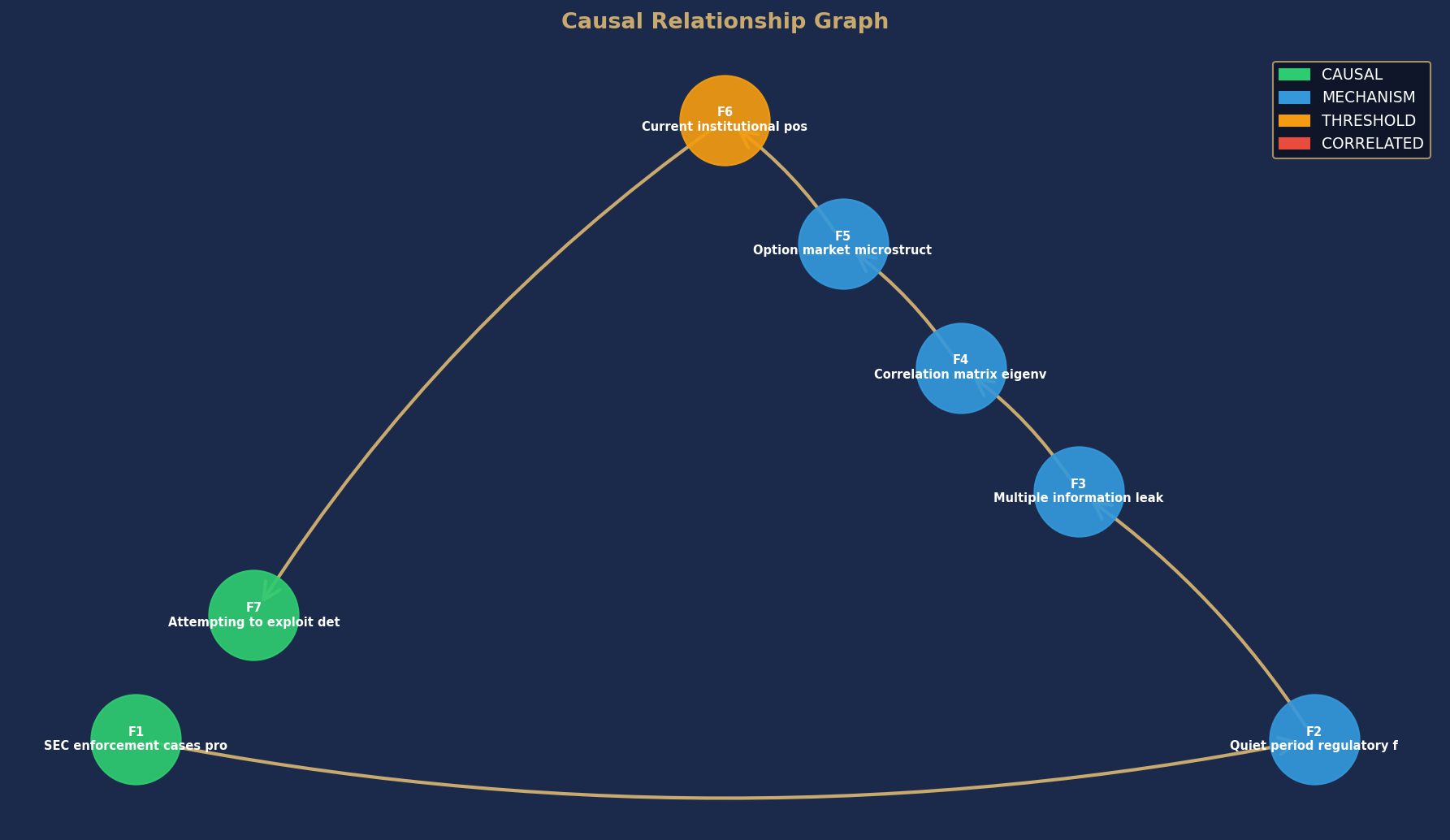

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Causal Analysis, Who Benefits and Why, Key Risks, and What to Watch are available in the full report.

Get the full analysis.

The full report includes the complete causal analysis with confidence ratings, differentiated beneficiary assessment, key risks, and specific data points to watch. Delivered as a PDF immediately after purchase.