CHINA'S IRAN GAMBIT: BILATERAL LEVERAGE, OIL STRATEGY, AND THE LIMITS OF STRAIT DISRUPTION AS STRATEGIC INSTRUMENT

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

CHINA'S IRAN GAMBIT: BILATERAL LEVERAGE, OIL STRATEGY, AND THE LIMITS OF STRAIT DISRUPTION AS STRATEGIC INSTRUMENT

Executive Summary

The most important finding in this analysis is the one that inverts the central premise of the question. China does not appear to be using negotiating silence or oil procurement strategy to signal a preference for prolonged Strait of Hormuz disruption. The observable evidence points to the opposite conclusion: Beijing is executing time-constrained risk management under mechanical energy constraints, selectively engaging with Washington while preserving optionality with Tehran, and treating the Strait crisis as a crisis to be managed rather than a condition to be prolonged.

The claim that bilateral China-US negotiations precede and structure multilateral Iran agreements is rated CORRELATED — the two channels operate simultaneously, not sequentially, and no mechanism has been confirmed linking bilateral terms to multilateral outcomes. The claim that Chinese oil import behavior signals a preference for extended disruption is rated THRESHOLD — the correlation exists but the proposed mechanism inverts causality. Strategic Petroleum Reserve accumulation of approximately 1.2 billion barrels is defensive preparation against disruption risk, not an indicator of preference for disruption. The claim that Chinese diplomatic silence signals commitment to prolonged Strait disruption is rated NOISE — Beijing has not been silent, it has been selectively engaging, and the signal type was misidentified.

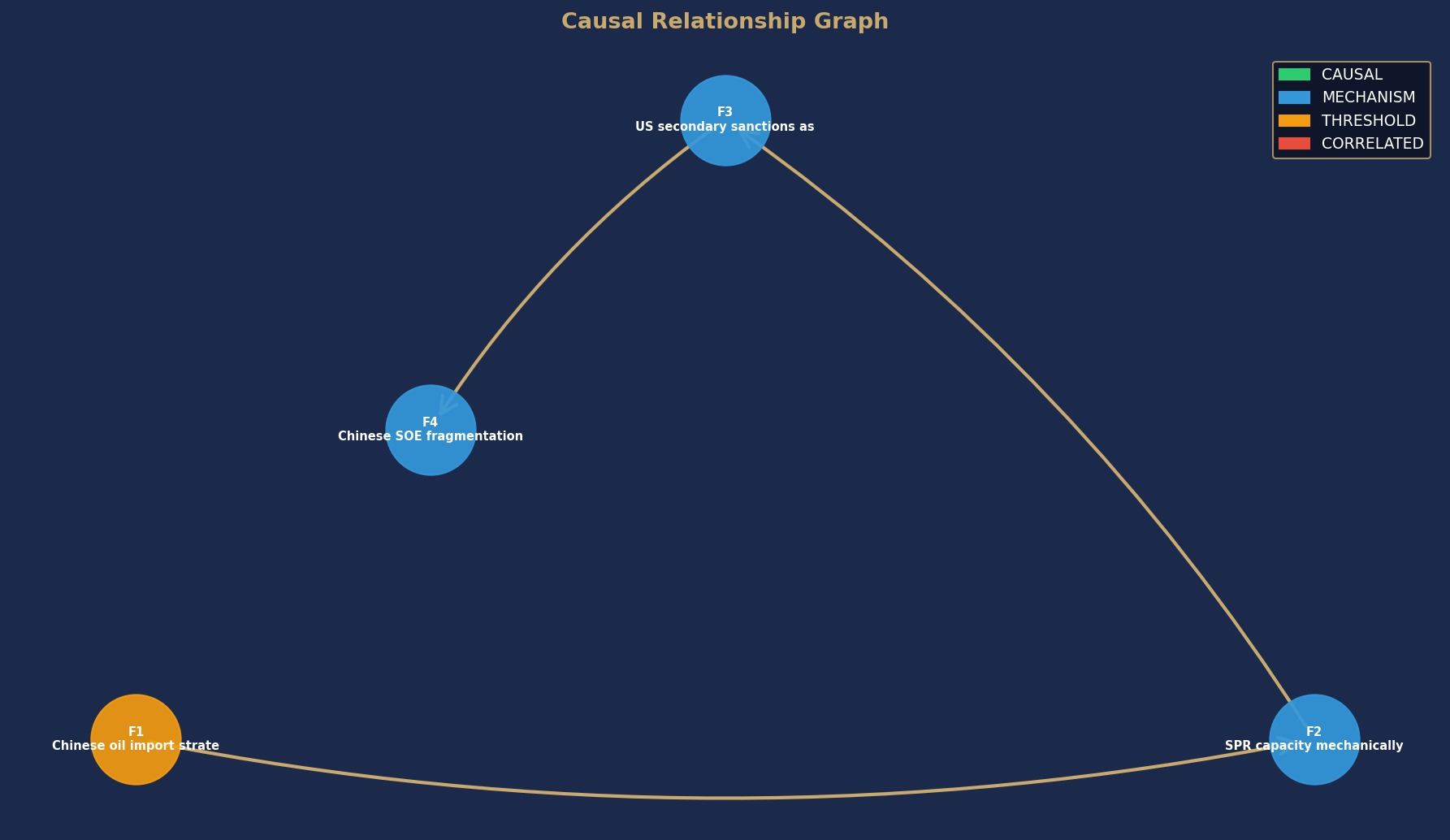

Three findings reach MECHANISM status and constitute the analytical core of this report. First, petroleum inventory arithmetic mechanically constrains China's ability to sustain any negotiating position that depends on Strait closure beyond approximately 60 to 120 days, regardless of strategic preference — and adversarial review suggests this window may extend further, to 180 to 300 days, if alternative non-Strait supply routes can be activated within existing contract capacity. Second, US secondary sanctions represent persistent, low-cost financial coercion, while Chinese Strait leverage is temporary and self-costly, but this asymmetry may partially reverse over a 180 to 360 day horizon if allied energy crises fracture US coalition cohesion. Third, institutional fragmentation among CNPC, Sinopec, and CNOOC produces behavior that cannot be read as the output of a unified Beijing disruption strategy, because competing institutional profit incentives explain observed procurement patterns without reference to geopolitical design.

The practical implication is significant. Analysts and policymakers treating Chinese behavior as a coherent disruption strategy are likely misreading decentralized risk management as centralized intent. The actionable indicator is not Chinese diplomatic statements, which are deliberately ambiguous, but Chinese SPR drawdown rates. When SPR depletion crosses the threshold that leaves fewer than 30 days of non-Strait import cover, Beijing's negotiating flexibility collapses regardless of stated preferences. That threshold, not any diplomatic calendar, determines the pace of resolution.

Situation and Context

The Iran crisis of 2026 emerged from a sequence of failures: collapsed nuclear negotiations in Geneva, a 12-day air conflict between Israel and Iran in 2025, and escalating Strait of Hormuz tensions that pushed Brent crude to approximately $126 per barrel in March 2026, the fastest oil price surge in any recent conflict period. [15] War-risk insurance premiums, which averaged roughly 0.25 percent of vessel value before the crisis, surged to between 3 and 8 percent, translating into insurance costs of $3 million to $8 million per tanker voyage. [52] Ships began seeking Iranian clearance to transit the Strait, a reversal of normal passage arrangements that underlined how thoroughly the operational environment had shifted. [53]

Against this backdrop, President Trump traveled to Beijing on May 14 and 15, 2026 for a bilateral summit with President Xi Jinping. Iran occupied a central position in the agenda alongside trade, technology, and Taiwan. [2] Xi reportedly offered diplomatic assistance in bringing the Iran conflict to a resolution, while ruling out any military assistance to parties in the conflict. [36] Trump publicly stated that Xi had offered help, but also stated he had not asked China for any specific favors on Iran, a formulation that reflects the deliberate ambiguity both sides were maintaining. [34]

China's position in the Iran energy system is structurally dominant. China purchases approximately 90 percent of Iran's oil exports. [12] Teapot refineries — China's network of independent, smaller-scale refinery operators concentrated in Shandong province — have served as the primary absorption mechanism for sanctioned Iranian crude, typically purchased through Malaysian blending intermediaries to obscure origin. [8] [13] The US Treasury and State Department escalated secondary sanctions pressure in April and May 2026, specifically targeting Chinese teapot refineries and warning international banks of sanctions exposure for any transactions involving these entities. [9] [10] [11] In response, China's state-owned oil majors Sinopec and CNPC suspended Iranian crude purchases for May, a visible tactical concession by the majors, though teapot purchasing remained ongoing through alternative channels. [39] [40]

China had assembled an estimated 1.2 billion barrels in its Strategic Petroleum Reserve by early 2026, equivalent to approximately 109 days of seaborne import cover. [Web search 2] This figure represents the culmination of an aggressive accumulation strategy that began accelerating in 2022 and continued through 2025 as Iran-Israel tensions escalated. The scale of this reserve is significant in both strategic and mechanical terms: it creates a buffer against Strait disruption but simultaneously defines the outer boundary of China's ability to operate independently of Strait access.

Iran's response to the stalled diplomatic environment has been to signal military readiness while expressing frustration with the pace of negotiations. Tehran media coverage following the Trump-Xi summit characterized the diplomatic situation as stalled, with growing internal concern that confrontation rather than resolution lay ahead. [32] [35] Iran had signaled willingness to repel new US attacks while simultaneously maintaining the posture of a party open to negotiated outcomes. This ambiguity on Iran's side mirrors the ambiguity Beijing maintains on its own.

The multilateral framework for Iran negotiations in 2026 lacks the structured architecture of the 2015 JCPOA process. China, Russia, and Iran held trilateral talks on the nuclear issue in Beijing, a format that serves legitimacy and information-sharing functions but does not constitute a negotiating mechanism with enforcement capacity. [27] [28] The House of Commons Library's 2026 briefing on Iran-US ceasefire and nuclear talks confirms that any path to agreement runs through bilateral US-Iran channels, with regional and great power participants playing facilitation rather than decision-making roles. [26]

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Causal Analysis, Who Benefits and Why, Key Risks, and What to Watch are available in the full report.

Get the full analysis.

The full report includes the complete causal analysis with confidence ratings, differentiated beneficiary assessment, key risks, and specific data points to watch. Delivered as a PDF immediately after purchase.