BEIJING'S TRIANGULAR PLAY: EXTRACTION STRATEGY, GENUINE RIVALRY, AND THE LIMITS OF PIVOTAL-STATE LEVERAGE

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

BEIJING'S TRIANGULAR PLAY: EXTRACTION STRATEGY, GENUINE RIVALRY, AND THE LIMITS OF PIVOTAL-STATE LEVERAGE

Executive Summary

The most important finding in this analysis is the one that reverses the conventional framing. Most commentary on Beijing's simultaneous courtship of Washington and Moscow treats China as the architect of a masterful pivot strategy, extracting unlimited concessions from desperate rivals. The evidence points to something more constrained and more interesting: Beijing is running a bounded extraction strategy within a genuinely competitive great-power rivalry, and the boundaries on that strategy matter as much as the strategy itself.

Three anchor findings drive this report.

First, Beijing is extracting real concessions through simultaneous high-profile diplomacy. The Trump-Xi summit of May 14, 2026, produced a "constructive relationship of strategic stability" framework and yielded restoration of EDA semiconductor design software access that had been blocked since May 2025. [5][46] Six days later, Xi and Putin signed fifteen-plus cooperation agreements deepening energy, technology, and trade ties. [7][10] The extraction is real. Rating: MECHANISM (causal mechanism identified; Stage 3 direct evidence that summits caused concessions, rather than independent policy dynamics, remains incomplete).

Second, the competition between Moscow and Washington for Chinese alignment is not theater. Both powers have concrete, structural reasons to court Beijing that predate and operate independently of Beijing's signaling. Russia depends on China as the residual buyer of sanctioned energy exports, having surpassed Saudi Arabia as China's top crude supplier at 1.86 million barrels per day in January 2026. [52] Washington needs to prevent Sino-Russian technological and military consolidation that would stress-test the entire Western sanctions architecture. These are not two nations performing rivalry for Beijing's benefit. They are two nations with incompatible strategic objectives competing on multiple fronts, with Chinese alignment representing a consequential but not singular prize. Rating: MECHANISM.

Third, and most importantly for decision-makers: the two findings above are not contradictory. Beijing is extracting within genuine rivalry, not manufacturing rivalry to enable extraction. The distinction matters enormously. If rivalry is genuinely structural, then Beijing's extraction capacity has a ceiling defined by structural asymmetries, not by Beijing's signaling sophistication. China cannot substitute for US semiconductor ecosystems. Russia cannot substitute for US financial system access. Beijing's room to maneuver is real but bounded.

The adversarial analysis conducted for this report identified a critical reasoning error that the initial domain analysis made, and which appears repeatedly in Western strategic commentary: mapping China's asymmetric dependencies is not the same as explaining Beijing's extraction strategy. Beijing's actual advantage is not that it faces no constraints. It is that Beijing faces asymmetric constraints in complementary domains, allowing sector-specific extraction from each power in domains where that power faces Beijing's leverage, not where Beijing faces the power's leverage. Against Russia, Beijing holds buyer-of-last-resort leverage on energy. Against the United States, Beijing holds supply-chain disruption and rare-earth denial leverage that is distinct from, and partially counterbalances, US semiconductor gatekeeping.

The practical implication: Beijing's extraction strategy has a 24-to-36-month sustainable horizon in its current form. Both the Trump-Xi framework ("next three years and beyond") [5] and the structural conditions enabling Beijing's balancing act face pressure from US Congressional semiconductor hawks, Russian energy-pricing dynamics, and the internal Chinese political cost of maintaining credible ambiguity to both domestic constituencies simultaneously.

Executives and analysts should treat managed competition as a transition state, not a durable equilibrium.

Situation and Context

On May 14, 2026, US President Donald Trump arrived in Beijing for his first state visit to China in nine years. [19] The visit followed a preliminary trade negotiation process described by both sides as having produced "generally balanced and positive results." [3] After summit-level talks at the Great Hall of the People, Xi Jinping and Trump agreed to build a "constructive China-US relationship of strategic stability," with this framework explicitly characterized by the Chinese Ministry of Foreign Affairs as providing "strategic guidance for China-US relations over the next three years and beyond." [17][23]

The summit produced specific commercial outcomes: agreements on soybean trade and rare earth elements, alongside confirmation that US firms could resume sales of electronic design automation software to Chinese chip designers, reversing restrictions that had been imposed in May 2025. [5][46] Xi used the meeting to deliver a public warning to Trump that Taiwan must be "handled properly" to avoid conflict, framing Taiwan as the single issue most capable of destabilizing the relationship. [6][21] On Iran, discussions were inconclusive but ongoing. [22]

Six days later, on May 20, 2026, Russian President Vladimir Putin arrived in Beijing for a separate state visit. [7][8] Putin and Xi signed a formal joint statement reaffirming commitment to deepening their "comprehensive strategic partnership," accompanied by fifteen cooperation agreements spanning energy, technology, trade, and strategic sectors. [7][10][16] Both governments framed the relationship as a "stabilizing force for global peace and prosperity" and explicitly described it as a model for major-country relations operating outside Western alliance structures. [14][15]

The back-to-back nature of these visits was not coincidental in its optics. Al Jazeera, citing analysts, described Beijing as holding the cards: a "neutral superpower" that both Washington and Moscow were competing to influence. [29] The sequencing placed Beijing in the enviable diplomatic position of having both rivals arrive as supplicants within the same week.

The structural context for this moment is a US-China trade relationship that has moved from acute tariff war through partial truce toward cautious stabilization. [1][2][4] Trade teams from both sides concluded preliminary negotiations before Trump's visit, with the summit itself serving as the ceremonial ratification of a framework negotiated at the working level. [4] The CNBC assessment characterized the outcome as a "stabilization" rather than a resolution, with core strategic tensions on Taiwan, technology transfer, and military competition left unaddressed. [18]

Meanwhile the Russia-China relationship has deepened materially since 2022. Russian crude exports to China reached more than 108 million tonnes in 2024, representing approximately a 30 percent increase since the Ukraine invasion. [52][53] By January 2026, Russia had displaced Saudi Arabia as China's largest crude supplier at 1.86 million barrels per day, a 46 percent year-on-year increase. [52] China now accounts for the dominant share of Russia's export revenue under a Western sanctions regime that has foreclosed most alternative markets. [56]

On the technology dimension, the US has maintained a layered export control architecture targeting advanced semiconductor nodes, while making selective concessions on adjacent products. EDA software restrictions were imposed in May 2025, creating disruptions at Siemens, Cadence, and Synopsys operations in China. [41][48] The partial reversal that followed [43][46] occurred in the period leading into the May 2026 summit, though the precise policy linkage between the reversal and diplomatic negotiations remains the subject of interpretive dispute. Advanced node restrictions remain in place. [42][49]

This is the environment in which Beijing is operating: genuine US-China economic interdependence at risk, genuine Russia-China energy interdependence expanding, and both the United States and Russia seeking Chinese accommodation for structurally different but equally urgent reasons.

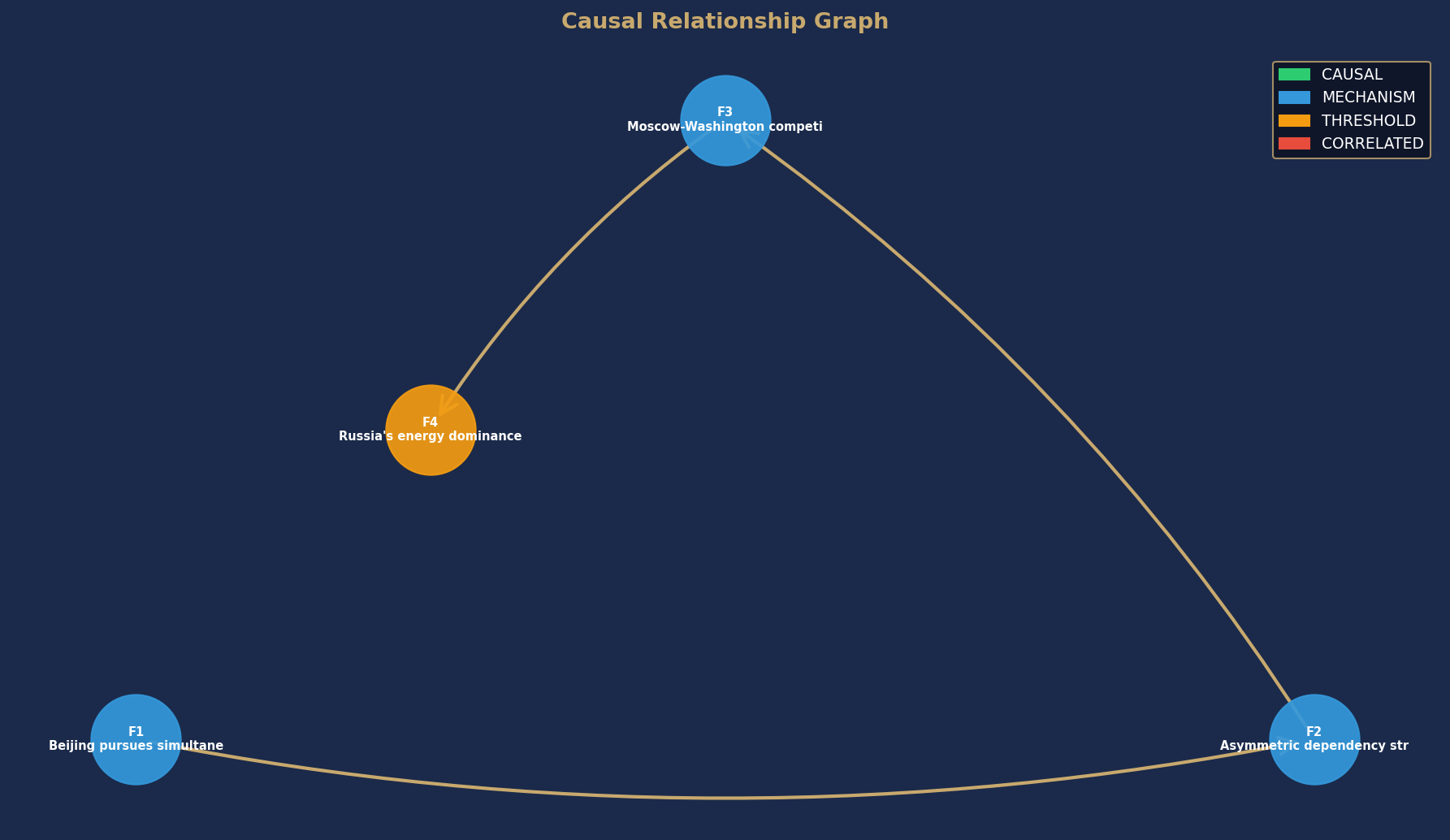

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Causal Analysis, Who Benefits and Why, Key Risks, and What to Watch are available in the full report.

Get the full analysis.

The full report includes the complete causal analysis with confidence ratings, differentiated beneficiary assessment, key risks, and specific data points to watch. Delivered as a PDF immediately after purchase.