FEDERAL RESERVE INSTITUTIONAL PARALYSIS RISK: HAWKISH OVERCOMPENSATION AS THE DOMINANT RESPONSE MODE, MAY 2026

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

FEDERAL RESERVE INSTITUTIONAL PARALYSIS RISK: HAWKISH OVERCOMPENSATION AS THE DOMINANT RESPONSE MODE, MAY 2026

Executive Summary

The non-obvious finding in this report is not that the Federal Reserve is paralyzed. It is not. The non-obvious finding is that the institutional stress currently concentrated in the Fed's governance structure produces a policy bias that is directionally opposite to paralysis: the intersection of geopolitical shock, leadership transition, and internal dissent is selectively amplifying hawkish voices while simultaneously stripping the incoming Chair of the authority needed to moderate that bias. The Fed enters the Warsh era not frozen, but pulled.

Four converging developments define the current situation. First, the April 2026 FOMC meeting produced four dissenting votes, the largest dissent count since 1992, on a statement that held rates steady but included forward guidance language implying the next move would be an easing. [11][14] Three of the four dissents were hawkish, opposing the easing signal rather than the rate hold itself. [13][79] Second, Kevin Warsh was confirmed on May 13, 2026 as the 17th Chair of the Federal Reserve in a 54-45 mostly party-line vote, the narrowest modern Chair confirmation in the post-Volcker era. [52][60] Third, the May 2026 Federal Reserve Financial Stability Report, released May 8, identified geopolitical risk and an oil price shock as the top concerns cited by survey respondents, with three-quarters naming geopolitical risk as a primary threat. [26] Fourth, options markets on May 13 showed the probability of a rate hike by December 2026 jumping from approximately 2 percent a month prior to 28 percent, driven by a combination of hot inflation data and the Warsh confirmation. [42]

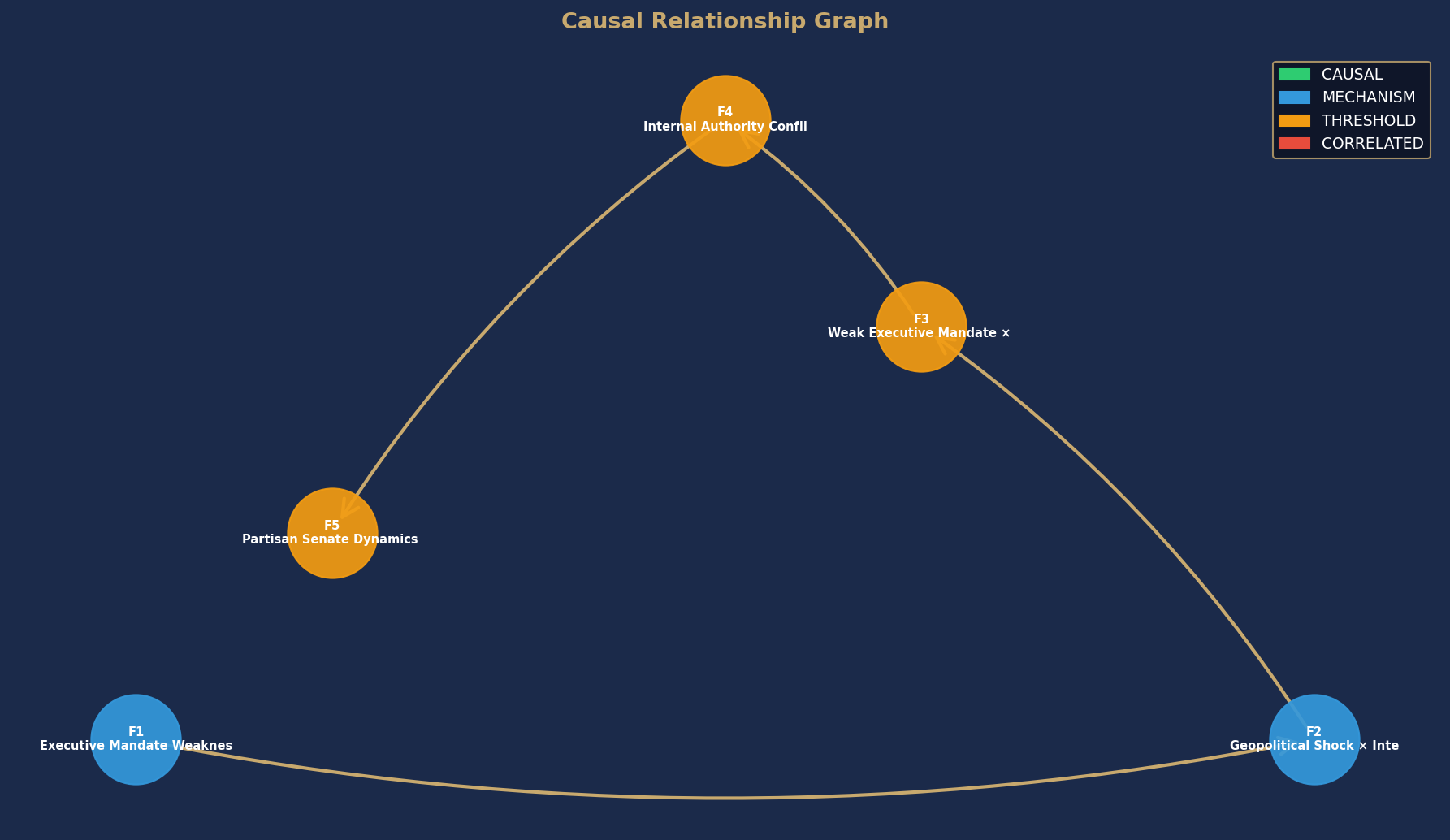

The causal analysis in this report, after adversarial review and independent verification, reaches the following rated conclusions. The mechanism by which weakened executive mandate reduces Chair disciplinary capacity and elevates the cost-benefit calculus for public dissent is supported at the MECHANISM level, not the CAUSAL level initially proposed. The primary causal alternative, that the March 2026 oil shock provided the exogenous trigger for April dissent while the leadership transition window provided permissive conditions, cannot be excluded. The geopolitical shock producing asymmetric incentives toward hawkish front-loading also rates MECHANISM: theoretically well-grounded and consistent with voting patterns, but not yet decomposed from competing causes of market repricing. Three findings rate THRESHOLD, meaning the correlation is robust and reproducible but the proximal mechanism remains underspecified. No finding in this analysis reaches the full CAUSAL standard.

The practical consequences of this rated framework are significant and should drive the report's utility. Market participants who treat the Fed's current communications as reflecting a single coherent institutional view are mispricing tail risks in both directions. The dominant policy trajectory points toward hawkish overcompensation, with the most likely scenario involving at least one rate increase before year-end 2026 driven by geopolitical inflation anxiety and credibility-restoration incentives for Warsh. The tail risk is not gridlock; it is an overcorrection that proves unnecessary if oil prices stabilize or decline, leaving the Fed exposed to accusations of cyclical damage from premature tightening.

The so-what for an executive, investor, or analyst is this: build positions that account for a Fed that is operationally functional but directionally biased hawkish, with an incoming Chair whose narrow confirmation mandate makes easing harder to execute than tightening. The policy error risk is not indecision. It is action taken with insufficient institutional ballast to course-correct.

Situation and Context

The Federal Reserve's current condition is the product of three overlapping structural stresses that have materialized simultaneously in the first half of 2026.

The first stress is the Iran war and its commodity market consequences. The conflict triggered a spike in West Texas Intermediate crude from approximately $55 per barrel before the conflict to over $90 per barrel by late March, with Brent crude briefly reaching $101.70. [62][64][67] Prices have since partially retreated to the $80-82 range as of May 2026. [78] The Federal Reserve's own semi-annual Financial Stability Report, released May 8, flagged geopolitical risk and the oil shock as the top systemic concerns, with three-quarters of respondents to the Fed's survey naming geopolitical risks as a primary worry. [24][26] San Francisco Fed President Mary Daly stated in April that the oil shock means getting inflation down will take longer, signaling that the transitory framing is losing support within the institution. [77] Minneapolis Fed President Neel Kashkari published analysis asking how long the Fed can look through the Iran war commodity shock before it becomes a persistent inflation threat. [65] Dallas Fed analysis examined the implications of the Iran war for US inflation directly. [66] The Morgan Stanley inflation warning regarding the Iran conflict and oil shock cited hawkish concerns as the dominant risk scenario. [45]

The second stress is the leadership transition. Jerome Powell's second term as Chair expired May 15, 2026. [53][56] Powell's final months were marked by what he described as a Department of Justice criminal indictment threat tied to his 2025 congressional testimony about a Fed building project, which he characterized in a January 11, 2026 statement as leaving him no practical choice but to remain in position through the end of his term. [35][38] Powell confirmed at the January 28 press conference that he would not seek early departure. [9] On April 29, his final FOMC meeting, Powell's statement passed with an 8-4 vote split. [18] Kevin Warsh, former Fed governor and Bush administration alumni, was nominated and confirmed on May 13, 2026 by a 54-45 vote, with only one Democratic senator, John Fetterman of Pennsylvania, voting in favor. [52][57][60] Powell announced he would remain on the Fed's Board of Governors as a regular member after stepping down as Chair. [53]

The third stress is the internal voting dynamics. The April 2026 meeting produced four dissenting votes on the FOMC statement, matching the highest dissent count since 1992. [11][79] Three dissents were hawkish: Beth Hammack, Neel Kashkari, and Lorie Logan opposed the inclusion of forward guidance suggesting the next rate move would be an easing. [13][79] One dissent was dovish, favoring a cut. [79] Earlier in January 2026, the FOMC also saw two dissenters, a hawkish shift from 2025 patterns. [16][80] February 2026 meeting minutes revealed that some members were not just resistant to cuts but open to hikes, a more extreme hawkish position than the formal dissent record captured. [83] The composition of the 2026 voting bloc includes several regionally-based Fed presidents with demonstrably hawkish communications records throughout 2025 and 2026. [81] Morningstar analysis characterized the FOMC as the most divided in recent history. [19]

What makes this situation analytically distinct from routine Fed turbulence is the coincidence of all three stresses within the same 90-day window. Leadership transitions have occurred before. Oil shocks have occurred before. Internal dissent has occurred before. What is rare is the simultaneous presence of all three, arriving precisely as the new Chair needs maximum institutional authority to impose coherent forward guidance on a divided committee.

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Causal Analysis, Who Benefits and Why, Key Risks, and What to Watch are available in the full report.

Get the full analysis.

The full report includes the complete causal analysis with confidence ratings, differentiated beneficiary assessment, key risks, and specific data points to watch. Delivered as a PDF immediately after purchase.