USTR SECTION 301: LEGAL REPOSITIONING OR TRADE POLICY ANALYSIS? ASSESSING INSTITUTIONAL INTENT AND STAKEHOLDER MISCALCULATION RISK IN THE 2026 TARIFF TRANSITION

IMPORTANT DISCLAIMER

This report is published by Novo Navis, LLC for general informational purposes only. It does not constitute financial advice, investment advice, legal advice, or any other professional advice. Nothing in this report should be construed as a recommendation to buy, sell, or hold any security, make any investment decision, or take any specific action.

The analysis contained in this report reflects information available as of May 2026. Market conditions, competitive dynamics, regulatory environments, and other factors can change rapidly. Novo Navis makes no representation that the information contained herein is accurate, complete, or current after the date of publication.

Always seek the advice of a qualified financial advisor, attorney, or other licensed professional before making decisions based on information in this report. Past performance of any market, company, or strategy referenced herein is not indicative of future results.

Novo Navis, LLC and its affiliates accept no liability for any loss or damage arising from reliance on this report.

USTR SECTION 301: LEGAL REPOSITIONING OR TRADE POLICY ANALYSIS? ASSESSING INSTITUTIONAL INTENT AND STAKEHOLDER MISCALCULATION RISK IN THE 2026 TARIFF TRANSITION

Executive Summary

The non-obvious finding in this analysis is that USTR's 2026 Section 301 investigations cannot be characterized as either pure trade policy analysis or pure legal repositioning — and that treating them as the former while ignoring the latter is the precise miscalculation likely to damage the most stakeholders.

When the Supreme Court invalidated IEEPA-based tariff authority on February 20, 2026, in a 6-3 decision, the administration faced a structural problem: approximately $166 billion in active duties had no surviving legal basis. [12][16] Within 21 days, USTR announced two sweeping Section 301 investigations targeting excess industrial capacity across 14 countries plus the EU, and forced labor enforcement failures across 59 countries plus the EU. [44][45] The pattern — same policy goals, different statutory vehicle, expedited deadline — is consistent with legal repositioning. But it is also consistent with competent contingency planning and ordinary institutional adaptation. The evidence does not permit a definitive verdict at causal certainty.

What the evidence does support, at mechanism-level confidence, is a directional claim: USTR selected Section 301 specifically because its statutory structure and the Chevron deference standard governing judicial review offer substantially lower legal vulnerability than the emergency powers framework the Supreme Court just rejected. Whether this reflects strategic evasion or sound institutional housekeeping is a question of intent — and intent is not directly observable in the public record.

Four findings emerge from the causal analysis:

First (MECHANISM, 55% confidence): USTR's rapid substitution of Section 301 for invalidated IEEPA authority is directionally consistent with legal repositioning. The mechanism — statutory permissiveness, Chevron deference, expedited deadline signaling intent to establish durable authority before judicial challenge ripens — is plausible and directional. But alternative explanations, including institutional compulsion and pre-planned contingency, cannot be ruled out. This finding is not actionable as a definitive characterization of USTR intent, but it is material for litigants assessing whether to mount judicial challenges.

Second (CORRELATED): USTR's reliance on qualitative rather than econometric injury analysis is real, but it reflects Section 301's statutory design rather than a deliberate choice to minimize falsifiable claims. The analytical sparsity cannot be attributed to legal durability strategy without a historical baseline showing standards have declined. This finding does not support the inference that USTR investigations are substantively hollow.

Third (MECHANISM, 60% confidence): Tier-2 suppliers and SME importers face material asymmetric information disadvantages during the February 20 to July 24, 2026 transition window. The mechanism — unequal access to legal expertise and USTR engagement channels, inability to model decision probability and timing — is theoretically sound and consistent with structural features of the regulatory environment. Empirical validation through actual trading data is absent, but the practical exposure is sufficiently plausible to warrant protective action by affected parties.

Fourth (MECHANISM, 75% confidence): The forced labor investigation rests on a standard trade economics mechanism — forced labor suppresses input costs, which depresses export prices, which causes U.S. producer injury — but USTR has not publicly quantified this chain. The mechanism exists; USTR's evidentiary rigor in documenting it remains uncertain.

The so-what for decision-makers: The July 24, 2026 investigation deadline is the single most important date in the current tariff landscape. Stakeholders who treat the outcome as uncertain and hedge accordingly will outperform those who assume Section 301 tariffs are either inevitable or easily challenged. The legal transition period is genuinely uncertain, and that uncertainty is asymmetrically costly to parties without legal resources to navigate it.

Situation and Context

On February 20, 2026, the Supreme Court issued its decision in Learning Resources, Inc. v. Trump, holding 6-3 that the International Emergency Economic Powers Act does not authorize the President to impose tariffs. [12][53] The ruling eliminated approximately $166 billion in active duties, including the broad reciprocal tariffs and fentanyl-related tariffs that had been the primary trade enforcement tool of the second Trump administration. [16][19] Chief Justice Roberts delivered the majority opinion. The Court's six-three split reflected the politically significant nature of the decision, but the legal rationale — IEEPA's text and legislative history do not support tariff imposition as an emergency power — drew on statutory analysis that had been telegraphed in lower court dissents and academic commentary for months. [14][20]

The immediate administrative response was to implement a 10 percent global tariff under Section 122 of the Trade Act of 1974, effective February 2026. [28] Section 122 authorizes temporary surcharges in response to balance-of-payments emergencies, but its 150-day statutory limit creates an expiration problem. The Court of International Trade has since invalidated the Section 122 tariffs as well, finding that the balance-of-payments predicate was not met. [17] That ruling is subject to appeal, adding a second layer of legal uncertainty to the post-IEEPA landscape.

The Section 301 investigations announced on March 12, 2026 represent the administration's most durable remaining trade enforcement vehicle. [44][45] USTR simultaneously initiated two distinct tracks. The first targets structural excess capacity and overproduction in manufacturing sectors across 14 economies plus the European Union — China, the EU, Singapore, Switzerland, Norway, Indonesia, Malaysia, Cambodia, Thailand, South Korea, Vietnam, Taiwan, Bangladesh, Mexico, and Japan among them. [47][24] The second targets failures to impose and effectively enforce prohibitions on forced labor imports across 59 economies plus the EU. [45][48] Both investigations were initiated under expedited procedures, with a stated intent to conclude before July 24, 2026. [2][30]

That date is not arbitrary. July 24, 2026 is the statutory deadline for the four-year review of existing China Section 301 tariff actions initiated in 2018. [4][21] USTR simultaneously launched the second four-year review of those tariffs in May 2026, initiating a second review process that will run in parallel with the new investigations. [21] The convergence of these deadlines concentrates an extraordinary amount of tariff policy consequence into a single calendar window.

Section 301 of the Trade Act of 1974 authorizes USTR to investigate foreign acts, policies, or practices that are unfair, unreasonable, or discriminatory and burden or restrict U.S. commerce. [13] Unlike Section 201 safeguard investigations, which require a formal injury determination by the International Trade Commission, Section 301 invests the investigative and determination authority in USTR itself. [7] This self-contained structure — USTR investigates, USTR determines, USTR recommends action — is one reason Section 301 tariffs have historically been more politically controllable than alternative trade remedies. It is also one reason they attract judicial scrutiny on arbitrary-and-capricious grounds: the same agency that wants the tariff also decides whether the predicate conditions are met. [52]

The current USTR investigation landscape thus includes four simultaneous active proceedings: the excess capacity investigation, the forced labor investigation, the second four-year review of China tariffs, and the ongoing Special 301 IP enforcement review cycle published in April 2026. [22][26] This is an unusually high-tempo investigative posture, particularly given that final determinations have not yet been issued in any of the major 2026 proceedings. [6]

Industry comment periods are open, with stakeholders across multiple sectors urged to submit evidence, data, and arguments before USTR closes the record. [8][2] The comment period structure creates a formal procedural record — essential for Chevron deference — but the evidentiary bar for what qualifies as sufficient documentation of injury has not been publicly specified. [9][10]

Causal Analysis

Finding One: Legal Repositioning — MECHANISM (55% Confidence)

The finding is that USTR's rapid substitution of Section 301 authority for invalidated IEEPA authority is directionally consistent with deliberate legal repositioning to establish tariff authority under a more deferential judicial review standard.

The correlation is real: IEEPA authority was invalidated February 20, Section 301 investigations targeting substantially similar policy objectives were announced March 12, and the expedited deadline of July 24 signals urgency to establish legal conclusions before judicial challenge becomes viable. [12][44][45] The statutory mechanism is directional: Section 301 investigations receive arbitrary-and-capricious review under Chevron deference, which requires courts to uphold USTR's interpretation of "trade practice" or "denial of rights" as long as it is reasonable. IEEPA tariffs faced strict scrutiny because the statute's scope was the issue before the Court, not the rationality of USTR's exercise of discretionary judgment. [13][51] The shift to Section 301 therefore substitutes a lower-scrutiny framework for a higher-scrutiny one.

The mechanism is directional but faces three material confounds that prevent a CAUSAL rating.

First, the alternative explanation of institutional compulsion is not ruled out. If IEEPA was eliminated and Section 122 was time-limited and legally contested, Section 301 was not a strategic choice — it was the remaining option. An agency substituting its last standing authority for an invalidated one is engaging in institutional adaptation, not necessarily strategic legal evasion. The domain analysis treated temporal proximity as causal evidence, but temporal proximity is equally consistent with constraint-driven response and competent contingency planning. [11]

Second, the "identical product categories" claim in earlier analysis was unsubstantiated. IEEPA tariffs targeted specific sectors — steel, electric vehicles, semiconductors, solar panels — while Section 301 excess capacity investigations target sectors by structural production dynamics across multiple countries. [47][5] These are related but not identical coverage areas. The correspondence is suggestive, not determinative.

Third, the evidence cited for Stage 3 causation — that investigations remain open without final determinations — is unfalsifiable as written. An ongoing investigation is open by definition until its statutory deadline. The openness of the proceeding cannot simultaneously serve as evidence that findings are strategically malleable and be the normal procedural state of any investigation. This logical error, identified in the adversarial review, prevents the finding from reaching CAUSAL status. [2][30]

What survives adversarial review: the mechanism is plausible, directional, and consistent with observable institutional incentives. USTR has a demonstrable interest in establishing durable authority that survives judicial review, and Section 301's Chevron-deferential framework offers that durability more reliably than emergency powers subject to strict statutory construction. [13][20] The temporal pattern is consistent with this mechanism operating. The mechanism rating reflects genuine uncertainty about intent, not weakness in the underlying legal analysis.

For litigants considering judicial challenges, this finding has practical implications. A Section 301 determination supported by a procedurally complete record — comment period, reasoned explanation, statutory predicate — will be substantially harder to overturn than the IEEPA tariffs were. The strategic value of that durability is real regardless of whether USTR consciously chose Section 301 for legal positioning or simply found it was the only viable remaining option.

Finding Two: Analytical Depth in Section 301 Investigations — CORRELATED

The correlation is real: USTR Section 301 investigations rely on qualitative harm narratives rather than econometric injury quantification. [3][23] The Federal Register notices initiating the excess capacity and forced labor investigations emphasize statutory authority and policy objectives rather than quantified measures of U.S. producer injury, price suppression magnitude, or employment displacement. [24][25]

This correlation does not support the inference that USTR deliberately deprioritized economic modeling to protect legal durability. The more parsimonious explanation is that Section 301 has never required quantification. The statute authorizes investigation of "unreasonable" practices; "unreasonable" is a qualitative judgment. [13] Unlike Section 201 safeguard investigations, which require the International Trade Commission to make affirmative injury findings on a quantified record, Section 301 vests the determination in USTR without specifying evidentiary standards. [7]

The adversarial review identified a critical missing element: no historical baseline establishes that prior Section 301 investigations were more econometrically rigorous. If the 2018 China Section 301 investigations — initiated under the first Trump administration — were equally qualitative, the current pattern reflects statutory design rather than strategic choice. [4][33] The knowledge base does not contain comparative data sufficient to establish a decline in analytical standards.

The finding is therefore CORRELATED: the qualitative orientation of USTR investigations is observable, but the proposed mechanism — legal durability incentives driving out quantification investment — is not established. Resource constraints and statutory design offer equally plausible explanations. This finding should not serve as a basis for characterizing USTR investigations as analytically hollow or for predicting judicial invalidation on inadequate-evidence grounds.

Finding Three: Tier-2 Supplier Miscalculation Risk — MECHANISM (60% Confidence)

The finding is that SME importers and tier-2 suppliers in supply chains exposed to the 14 excess capacity and 59 forced labor target countries face material asymmetric information disadvantages during the February 20 to July 24, 2026 transition window, creating financial exposure through suboptimal hedging, sourcing lock-in, and timing miscalculation.

The mechanism operates through three channels. First, probability miscalculation: tier-1 suppliers with in-house trade counsel can model USTR's Section 301 standards, assess the likelihood of final tariff imposition based on statutory interpretation and Chevron doctrine, and calibrate hedging decisions accordingly. Tier-2 suppliers without legal resources rely on public signals — USTR press releases, media reporting — that do not permit the same probabilistic assessment. [9][10] Second, timing miscalculation: the July 24 deadline is public, but the actual announcement timing of final determinations is discretionary and may be conditioned on political or negotiating considerations rather than investigative completion. Tier-2 suppliers cannot access non-public USTR decision timelines and must assume uniform probability across the window. Third, category exposure miscalculation: USTR investigations target broad country sets without product-level specificity until final determination. Tier-2 suppliers in intermediate goods or component supply chains cannot determine whether their inputs fall within scope, making sourcing diversification decisions irreducibly uncertain. [5][46]

The mechanism is theoretically sound and grounded in the structural features of USTR's investigative process. The information asymmetry between parties with USTR comment-period access and those relying on public announcements is a real and documented feature of Section 301 proceedings. [8][54]

The finding does not reach CAUSAL status for a specific reason: the empirical evidence cited in the domain analysis of actual differentiated trading behavior — measurable differences in inventory positioning and hedging decisions between tier-1 and tier-2 suppliers during this transition window — is not provided in the source record. The educational framework in the knowledge base documents the asymmetry in theoretical terms; the trading data that would confirm it operates in the specific February-July 2026 window is identified as a critical evidence gap. [GAP_003] The Section 122 tariff application as evidence that tier-2 suppliers were "caught unprepared" also involves a category error: the government's decision to implement a tariff is administrative action, not evidence of market participant miscalculation.

For supply chain risk managers, the mechanism-level confidence is still material for practical decision-making. The absence of empirical confirmation does not eliminate the structural exposure — it means the magnitude of losses cannot be quantified in advance, not that the exposure is zero.

Finding Four: Forced Labor Trade Practice Mechanism — MECHANISM (75% Confidence)

The finding that the forced labor investigation lacks an identifiable trade injury mechanism was overstated in prior analysis. The standard economic chain — forced labor suppresses labor input costs, which lowers production costs, which depresses export prices, which causes U.S. producer injury through price competition — is a textbook trade economics mechanism that does not require USTR quantification to be identifiable. [9][23]

The domain analysis made a logical error by conflating two distinct questions: whether a causal mechanism linking forced labor to U.S. trade injury exists, and whether USTR has quantified that mechanism in its investigation file. These are separate questions. The forced labor investigation sits at MECHANISM rather than THRESHOLD because the price suppression channel is plausible, directional, and consistent with established trade economics, even though USTR's investigative documentation does not appear to have quantified it. [45][48]

What this means practically: the forced labor investigation is not legally baseless. Courts applying Chevron deference can accept USTR's determination that forced labor constitutes a "denial of rights" or "unreasonable trade practice" under Section 301 without requiring a fully quantified injury analysis. The judicial vulnerability of the forced labor track is therefore lower than the domain analysis originally suggested — though it remains higher than the excess capacity track, where the capacity-to-price-injury mechanism is more straightforwardly documented in trade economics literature. [5][27]

The residual uncertainty at 25% reflects the evidentiary challenge: if a plaintiff demonstrates that USTR's actual investigation file contains only statutory recitation and no factual development of the price injury mechanism, an arbitrary-and-capricious challenge becomes viable even under deferential review. [51][52] The strength of Section 301 forced labor determinations will depend significantly on what USTR actually places in the record during the comment period.

Who Benefits and Why

Large Multinational Importers with USTR Access — Net Beneficiary During Transition (MECHANISM)

Tier-1 importers — large multinationals, major retailers, and industry associations with dedicated trade counsel — benefit asymmetrically from the current transition period. Their advantage operates through three channels. First, they participate directly in USTR comment periods, providing them non-public signals about investigative scope, preliminary findings, and likely tariff list composition before final determinations are announced. [8][54] Second, they can model the Chevron deference standard with precision, estimating the probability of successful judicial challenge and calibrating hedging decisions accordingly. Third, their established relationships with alternative sourcing jurisdictions enable faster supply chain repositioning in response to tariff signals. The mechanism confidence is 60%, matching Finding Three — the information asymmetry structural feature is real, but magnitude of advantage is unquantified.

Time horizon: Immediate (February–July 2026 window).

Domestic U.S. Producers in Excess Capacity Sectors — Conditional Beneficiary (MECHANISM)

U.S. producers in steel, aluminum, electric vehicles, semiconductors, solar, and similar sectors targeted by the excess capacity investigation stand to benefit if USTR issues final tariffs. The causal chain — Section 301 tariffs raise import prices, reducing foreign competition, improving domestic price realization — is straightforward. [23][27][32] However, this benefit is conditional on two factors that are currently unresolved: whether USTR issues final determinations before July 24, and whether those determinations survive judicial challenge under the arbitrary-and-capricious standard. Domestic producers who have already made capital allocation decisions on the assumption that tariffs will be implemented face potential losses if final determinations are delayed or legally challenged.

Time horizon: Medium-term (second half 2026, contingent on final determinations).

Legal Services Sector and Trade Counsel — Certain Beneficiary (CAUSAL)

The demand for trade law services is structurally elevated by the current environment. Four simultaneous USTR investigations, active judicial challenges to Section 122 tariffs, a pending Supreme Court petition on China Section 301 tariffs, and the IEEPA invalidation's downstream effects all generate billable work. [11][15][52] Trade counsel representing tier-1 importers during comment periods, litigants challenging Section 301 tariffs on arbitrary-and-capricious grounds, and supply chain consultants repositioning sourcing are all experiencing demand-driven revenue increases. This is CAUSAL: the proliferation of unsettled legal questions directly generates demand for legal and advisory services.

Time horizon: Immediate and ongoing.

Tier-2 Suppliers and SME Importers in Targeted Supply Chains — Material Loser (MECHANISM)

The information asymmetry mechanism establishes that SME importers and tier-2 suppliers in supply chains exposed to the 14 excess capacity and 59 forced labor target countries face suboptimal hedging and sourcing decisions relative to their tier-1 counterparts. [9][10][31] The specific exposure categories: procurement cycle lock-in (companies with 6-to-12-month sourcing commitments cannot rapidly diversify away from tariffed jurisdictions), inventory timing miscalculation (neither over-hedging before final determinations nor under-hedging to avoid sunk costs is optimal without knowing the determination date), and tariff-rate uncertainty (without product-level scope information, cost modeling for FY2026 planning is unreliable).

Time horizon: Immediate (February–July 2026); extending into late 2026 for sourcing repositioning.

U.S. Trading Partners in Both Investigation Tracks — Bifurcated Risk (CORRELATED)

Countries facing excess capacity investigations — particularly China, the EU, and Southeast Asian manufacturing economies — face potential tariff imposition that would reduce U.S. market access. [47][5] The correlation between investigation and eventual tariff imposition is observable from prior Section 301 history, but whether USTR will issue final tariffs at all (rather than accepting negotiated commitments) is uncertain. Countries that negotiate bilateral frameworks with the administration before July 24 may convert tariff risk into negotiated outcomes with reduced trade disruption. The EU in particular faces simultaneous exposure in both the excess capacity and forced labor tracks, concentrating its diplomatic and legal vulnerability. [44][45][46]

Time horizon: Medium-term (second half 2026).

Key Risks

Risk One: Section 301 Investigations Are Also Judicially Invalidated

The analysis rests on the assumption that Section 301 authority is more durable than IEEPA under judicial review. This assumption is directionally supported but not empirically confirmed. The pending Supreme Court petition on China Section 301 tariff litigation demonstrates that this authority is actively contested. [15] If the Supreme Court grants certiorari and applies non-delegation doctrine analysis — examining whether Congress gave USTR an intelligible principle to guide its Section 301 determinations — the excess capacity and forced labor investigations could face the same structural challenge that eliminated IEEPA authority. [51] If this resolved adversely, the core MECHANISM finding about legal repositioning would be undermined: USTR would have substituted one legally vulnerable authority for another, with the same eventual outcome.

Risk Two: USTR Fails to Meet July 24 Deadline

The expedited timeline is USTR's asserted intent, not a statutory requirement. Final determinations have not been issued in either the excess capacity or forced labor tracks as of May 2026. [6] If USTR delays determinations beyond July 24, the strategic value of the expedited timeline — establishing durable authority before legal challenges ripen — is reduced, and the policy window may close with negotiated agreements substituting for formal tariff determinations. This would affect the calculus for all stakeholders who have made hedging or sourcing decisions premised on tariff imposition.

Risk Three: Tier-2 Supplier Exposure Is Overstated Due to Symmetric Constraints

The tier-2 supplier miscalculation risk finding depends on the information asymmetry being specifically asymmetric between tier-1 and tier-2 suppliers. If the 21-day window between IEEPA invalidation and Section 301 announcement constrained all market participants symmetrically — as the adversarial review noted is possible — tier-2 suppliers may not be disproportionately exposed relative to tier-1 suppliers. [GAP_003] This risk does not eliminate the practical exposure of tier-2 suppliers, but it would reduce the confidence that the exposure is specifically asymmetric rather than market-wide.

Risk Four: Comment Period Record Does Not Support Final Determinations

The quality of USTR's investigation record — the evidentiary foundation placed in the file during the comment period — directly determines the strength of final determinations under arbitrary-and-capricious review. [52][8] If comment periods generate sparse or adversarial records, and USTR issues final tariffs on thin evidentiary grounds, judicial challenges citing inadequate factual basis have a viable path. This risk is specifically elevated for the forced labor track, where the price injury mechanism has not been publicly quantified. Plaintiffs challenging those tariffs would argue that USTR cannot demonstrate a rational connection between the statutory predicate and the tariff remedy — the core Chevron Step 2 vulnerability.

What to Watch

The July 24, 2026 deadline is the single most important observable trigger. Watch whether USTR issues final determinations before, on, or after this date — and whether those determinations are accompanied by product-level tariff lists or are issued at the sector or country level. Product-level specificity will be the key indicator of how carefully USTR has calibrated legal durability versus policy breadth.

Watch the Supreme Court's disposition of the pending Section 301 petition on China tariff litigation. [15] A decision to grant certiorari would signal that the Court views Section 301 authority as the next legal frontier after IEEPA, materially increasing judicial risk for the 2026 investigations before final determinations are even issued.

Watch the appellate outcome of the Court of International Trade's Section 122 invalidation. [17] If the Federal Circuit upholds the CIT and the Section 122 tariffs are also eliminated, the administration's remaining tariff authority is concentrated almost entirely in Section 301 and Section 232. That concentration would increase both the political and legal pressure on Section 301 determinations, affecting both the administration's urgency to finalize investigations and litigants' incentives to challenge them.

Watch EU and China diplomatic engagement with USTR between now and July 24. Negotiated bilateral frameworks, if offered, would indicate that the administration values a settled outcome over a contested final determination — a signal that the legal durability of Section 301 authority is less certain than the public record suggests.

Finally, watch USTR's comment period record for the excess capacity and forced labor investigations. The number of substantive economic submissions, the quality of injury documentation, and USTR's public responses to adverse comments will be leading indicators of whether the final investigation record can withstand arbitrary-and-capricious review.

APPENDIX: ANALYSIS LOG

Report ID: NN-2026-0512-USTR-S301

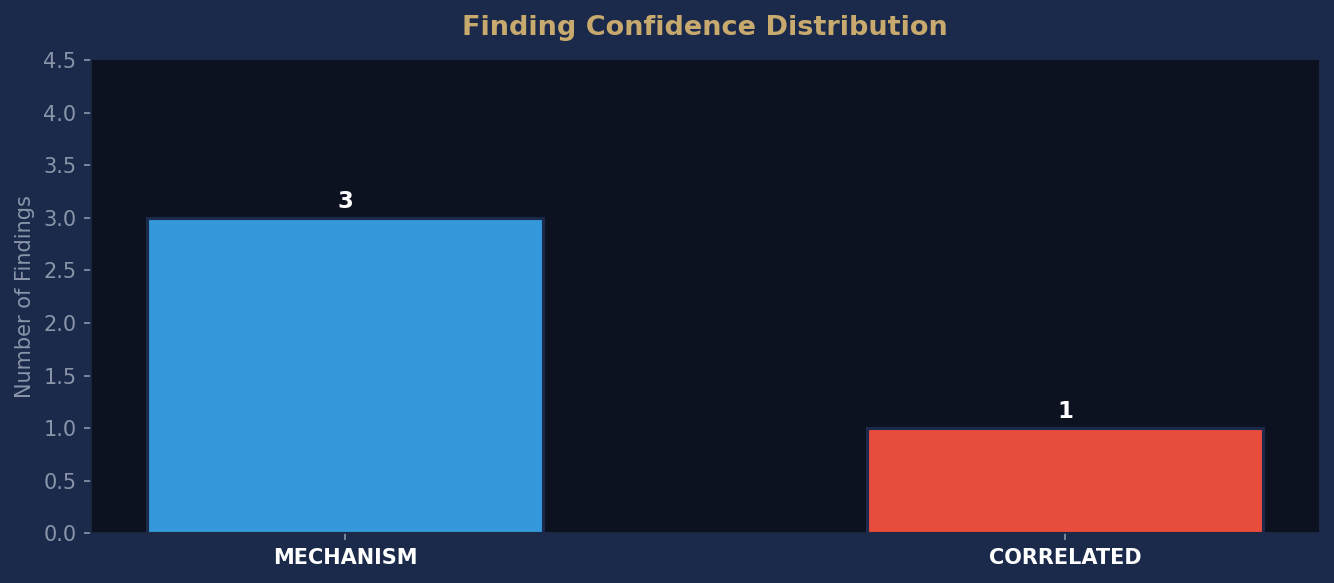

Topic: Whether USTR Section 301 investigations constitute substantive trade policy analysis or deliberate legal repositioning, and identification of stakeholders facing material miscalculation risk during the legal transition period Published: May 2026 Real-time data gathered: Yes Sources cited: 58 Causal ratings: CAUSAL 0 | MECHANISM 3 | THRESHOLD 0 | CORRELATED 1 Verification agreements: 3 | Overrides: 0 Open questions: GAP_001: Real-time docket-level documentation from March-May 2026 USTR investigations showing investigative depth metrics, comment volume, and economic modeling rigor — would resolve whether analytical sparsity reflects statutory design or deliberate deprioritization GAP_002: Specific judicial review precedent from the February 2026 Supreme Court decision defining arbitrary-and-capricious standards as applied to Section 301 determinations post-IEEPA invalidation — would clarify the actual legal durability differential between Section 301 and invalidated IEEPA authority GAP_003: Quantified stakeholder hedging data and supply chain repositioning volumes during February-May 2026 transition — would confirm or refute tier-2 asymmetric miscalculation exposure and permit magnitude assessment

Bibliography

[1] Why USTR’s Latest Section 301 Actions Matter for Your Supply Chain https://www.morganlewis.com/pubs/2026/04/why-ustrs-latest-section-301-actions-matter-for-your-supply-chain Accessed: 2026-05-12T08:00:57.613596

[2] Answering the Top Seven Questions About Pending Section 301 Deadlines | Crowell & Moring LLP https://www.crowell.com/en/insights/client-alerts/answering-the-top-seven-questions-about-pending-section-301-comment-deadlines Accessed: 2026-05-12T08:00:57.613596

[3] Section 301 Investigation into Brazil’s Acts, Policies, and Practices | Congress.gov | Library of Congress https://www.congress.gov/crs-product/IN12613 Accessed: 2026-05-12T08:00:57.613596

[4] Four-Year Review | United States Trade Representative

https://ustr.gov/trade-topics/enforcement/section-301-investigations/section-301-china-technology-transfer/china-section-301-tariff-actions-and-exclusion-process/four-year-review Accessed: 2026-05-12T08:00:57.613596

[5] USTR Launches Broad Section 301 Investigations Into Excess Supply, Forced Labor Prohibitions | Davis Wright Tremaine https://www.dwt.com/insights/2026/03/ustr-launches-broad-section-301-investigations Accessed: 2026-05-12T08:00:57.613596

[6] USTR to review China tariffs as Section 301 takes center stage | Supply Chain Dive https://www.supplychaindive.com/news/ustr-to-review-china-tariffs-as-section-301-takes-center-stage/819497/ Accessed: 2026-05-12T08:00:57.613596

[7] Section 301 Investigations | United States Trade Representative

https://ustr.gov/issue-areas/enforcement/section-301-investigations Accessed: 2026-05-12T08:00:57.613596

[8] USTR urged to proceed with caution on Section 301 actions https://www.feedstuffs.com/policy/ustr-urged-to-proceed-with-caution-on-section-301-actions Accessed: 2026-05-12T08:00:57.613596

[9] USTR Section 301 Forced Labor Investigations: Tariff Risk, UFLPA Overlap, and What Companies Should Do Now | News & Insights | Arnall Golden Gregory LLP https://www.agg.com/news-insights/publications/ustr-section-301-forced-labor-investigations-tariff-risk-uflpa-overlap-and-what-companies-should-do-now/ Accessed: 2026-05-12T08:00:57.613596

[10] Section 301 Investigations 2026: What Importers Need to Know | Fleischer Group https://www.fleischer-chb.com/post/new-section-301-investigations-what-importers-need-to-know-now Accessed: 2026-05-12T08:00:57.613596

[11] Duane Morris LLP - New Section 301 Investigations, IEEPA Tariff Refund Developments and Legal Challenges to Section 122 Tariffs – What Businesses Need to Know https://www.duanemorris.com/alerts/new_section_301_investigations_ieepa_tariff_refund_developments_legal_challenges_section_0426.html Accessed: 2026-05-12T08:01:07.833813

[12] Supreme Court Strikes Down IEEPA Tariffs—What Now?

https://www.wilmerhale.com/en/insights/client-alerts/20260220-supreme-court-strikes-down-ieepa-tariffs-what-now Accessed: 2026-05-12T08:01:07.833813

[13] Section 301 of the Trade Act of 1974 | Congress.gov | Library of Congress https://www.congress.gov/crs-product/IF11346 Accessed: 2026-05-12T08:01:07.833813

[14] Supreme Court Shakes Up Tariff Rules | Seyfarth Shaw LLP https://www.seyfarth.com/news-insights/supreme-court-shakes-up-tariff-rules.html Accessed: 2026-05-12T08:01:07.833813

[15] Plaintiffs in China Section 301 Tariff Litigation File Petition with U.S. Supreme Court Seeking Review of Federal Circuit Decision | SmarTrade https://www.thompsonhinesmartrade.com/2026/02/plaintiffs-in-china-section-301-tariff-litigation-files-petition-with-supreme-court-seeking-review-of-federal-circuit-decision/ Accessed: 2026-05-12T08:01:07.833813

[16] Supreme Court Strikes Down IEEPA Tariffs—Key Takeaways and Implications for Importers | Insights | Ropes & Gray LLP https://www.ropesgray.com/en/insights/alerts/2026/02/supreme-court-strikes-down-ieepa-tariffs-key-takeaways-and-implications-for-importers Accessed: 2026-05-12T08:01:07.833813

[17] U.S. Court of International Trade Invalidates the Administration's Section 122 Tariffs | Insights | Holland & Knight https://www.hklaw.com/en/insights/publications/2026/05/us-court-of-international-trade-invalidates-the-administrations Accessed: 2026-05-12T08:01:07.833813

[18] TARIFFS UPDATE: What You Need to Know About That Big Supreme Court Decision | Specialty Equipment Market Association (SEMA) https://www.sema.org/news-media/enews/2026/09/tariffs-update-what-you-need-know-about-big-supreme-court-decision Accessed: 2026-05-12T08:01:07.833813

[19] Post-IEEPA Tariff Landscape: New Authorities and the Path to Refunds | Freshfields https://blog.freshfields.us/post/102mn2g/post-ieepa-tariff-landscape-new-authorities-and-the-path-to-refunds Accessed: 2026-05-12T08:01:07.833813

[20] Trump's latest tariffs in court: Are they about to be blocked? | PIIE https://www.piie.com/blogs/realtime-economics/2026/trumps-latest-tariffs-court-are-they-about-be-blocked Accessed: 2026-05-12T08:01:07.833813

[21] USTR Initiates Second Four-Year Review of Section 301 Tariff Actions on Imports of Certain Chinese Products | SmarTrade https://www.thompsonhinesmartrade.com/2026/05/ustr-initiates-second-four-year-review-of-section-301-tariff-actions-on-imports-of-certain-chinese-products/ Accessed: 2026-05-12T08:01:15.892258

[22] USTR Releases 2026 Special 301 Report on Intellectual Property Protection and Enforcement | United States Trade Representative https://ustr.gov/about/policy-offices/press-office/press-releases/2026/april/ustr-releases-2026-special-301-report-intellectual-property-protection-and-enforcement Accessed: 2026-05-12T08:01:15.892258

[23] The 2026 Strategic Reorientation of American Trade Policy: Addressing Structural Excess Capacity and Global Overproduction through Section 301 – DSAP Law Firm https://www.dsaplawfirm.com/en/2026/03/13/the-2026-strategic-reorientation-of-american-trade-policy-addressing-structural-excess-capacity-and-global-overproduction-through-section-301/ Accessed: 2026-05-12T08:01:15.892258

[24] Federal Register :: Initiation of Section 301 Investigations: Acts, Policies, and Practices of Certain Economies Relating to Structural Excess Capacity and Production in Manufacturing Sectors https://www.federalregister.gov/documents/2026/03/17/2026-05214/initiation-of-section-301-investigations-acts-policies-and-practices-of-certain-economies-relating Accessed: 2026-05-12T08:01:15.892258

[25] Federal Register :: Initiation of Section 301 Investigations of Acts, Policies, and Practices of Various Economies Related to the Failure To Impose and Effectively Enforce a Prohibition on the Importa https://www.federalregister.gov/documents/2026/03/17/2026-05151/initiation-of-section-301-investigations-of-acts-policies-and-practices-of-various-economies-related Accessed: 2026-05-12T08:01:15.892258

[26] 2026 Special 301 Report Office of the United States Trade Representative https://ustr.gov/sites/default/files/files/Press/Releases/2026/2026%20Special%20301%20Report.pdf Accessed: 2026-05-12T08:01:15.892258

[27] Fact Sheet: USTR Initiates Section 301 Investigations into Structural Excess Capacity and Production in Manufacturing Sectors | United States Trade Representative https://ustr.gov/about/policy-offices/press-office/fact-sheets/2026/march/fact-sheet-ustr-initiates-section-301-investigations-structural-excess-capacity-and-production Accessed: 2026-05-12T08:01:15.892258

[28] U.S. tariffs: IEEPA refunds, what comes next, and how to prepare | Our Insights | Plante Moran https://www.plantemoran.com/explore-our-thinking/insight/2026/03/us-tariffs-what-comes-next Accessed: 2026-05-12T08:01:25.705363

[29] US Tariffs 2026: Section 301, IEEPA, 232 | Suaid Global https://suaidglobal.com/insights/us-tariffs-2026-guide/ Accessed: 2026-05-12T08:01:25.705363

[30] Section 301 Tariffs 2026: What Every Importer Must Know Before July 24 2026 - Carra Globe https://carraglobe.com/section-301-tariffs-2026/ Accessed: 2026-05-12T08:01:25.705363

[31] The New Tariff Reality: What U.S. importers face in 2026 - Logistics Management https://www.logisticsmgmt.com/article/the_new_tariff_reality_what_u.s_importers_face_in_2026 Accessed: 2026-05-12T08:01:25.705363

[32] Section 301 Tariffs Explained: Complete List & Rates 2025 https://content.ballastmarkets.com/blog/2025-11-08-section-301-tariffs-explained-complete-list/ Accessed: 2026-05-12T08:01:25.705363

[33] China Section 301-Tariff Actions and Exclusion Process | United States Trade Representative https://ustr.gov/issue-areas/enforcement/section-301-investigations/tariff-actions Accessed: 2026-05-12T08:01:25.705363

[34] U.S. trade developments: IEEPA tariffs end, but will new Section 301 tariffs follow? https://www.blg.com/en/insights/2026/03/us-trade-developments-ieepa-tariffs-end-but-will-new-section-301-tariffs-follow Accessed: 2026-05-12T08:01:25.705363

[35] The United States-Mexico-Canada Agreement: Settlement of Disputes | Baker Institute https://www.bakerinstitute.org/research/united-states-mexico-canada-agreement-settlement-disputes Accessed: 2026-05-12T08:01:32.790720

[36] WTO Law vs. U.S. Trade Act Section 301: A Legal and Economic Conflict | TaxTMI https://www.taxmanagementindia.com/visitor/detail_article.asp?ArticleID=13576 Accessed: 2026-05-12T08:01:32.790720

[37] 33.214 Alternative dispute resolution (ADR). | Acquisition.GOV

https://www.acquisition.gov/far/33.214 Accessed: 2026-05-12T08:01:32.790720

[38] WTO | Alternative Dispute Resolution Procedures

https://www.wto.org/english/tratop_e/dispu_e/mpia_e.htm Accessed: 2026-05-12T08:01:32.790720

[39] Dispute settlement mechanisms under the CPTPP and the RCEP - Global Arbitration Review https://globalarbitrationreview.com/review/the-asia-pacific-arbitration-review/2023/article/dispute-settlement-mechanisms-under-the-cptpp-and-the-rcep Accessed: 2026-05-12T08:01:32.790720

[40] Dispute Settlement | USTR

https://ustr.gov/sites/default/files/TPP-Chapter-Summary-Dispute-Settlement.pdf Accessed: 2026-05-12T08:01:32.790720

[41] CPTPP Environment Chapter: Dispute Settlement Mechanism - International Economics https://tradeeconomics.com/cptpp-environment-chapter-dispute-settlement-mechanism/ Accessed: 2026-05-12T08:01:32.790720

[42] The Digital Markets, Competition and Consumers Act 2024 (Alternative Dispute) Regulations 2026 - GOV.UK https://www.gov.uk/government/publications/the-digital-markets-competition-and-consumers-act-2024-alternative-dispute-regulations-2026 Accessed: 2026-05-12T08:01:32.790720

[43] REFORMING INVESTMENT DISPUTE SETTLEMENT: A STOCKTAKING H I G H L I G H T S

https://unctad.org/system/files/official-document/diaepcbinf2019d3_en.pdf Accessed: 2026-05-12T08:01:32.790720

[44] USTR Initiates Section 301 Investigations Relating to Structural Excess Capacity and Production in Manufacturing Sectors | United States Trade Representative https://ustr.gov/about/policy-offices/press-office/press-releases/2026/march/ustr-initiates-section-301-investigations-relating-structural-excess-capacity-and-production Accessed: 2026-05-12T08:02:37.087183

[45] USTR Initiates 60 Section 301 Investigations Relating to Failures to Take Action on Forced Labor | United States Trade Representative https://ustr.gov/about/policy-offices/press-office/press-releases/2026/march/ustr-initiates-60-section-301-investigations-relating-failures-take-action-forced-labor Accessed: 2026-05-12T08:02:37.087183

[46] New Section 301 Investigations on Countries Regarding Manufacturing Overcapacity and Forced-Labor Enforcement | Insights | Mayer Brown https://www.mayerbrown.com/en/insights/publications/2026/03/new-section-301-investigations-on-countries-with-manufacturing-overcapacity-and-forced-labor-enforcement Accessed: 2026-05-12T08:02:37.087183

[47] USTR initiates Section 301 investigations of 16 US trade partners targeting industrial excess capacity | White & Case LLP https://www.whitecase.com/insight-alert/ustr-initiates-section-301-investigations-16-us-trade-partners-targeting-industrial Accessed: 2026-05-12T08:02:37.087183

[48] Fact Sheet: USTR Initiates 60 Section 301 Investigations Relating to Failures to Take Action on Forced Labor | United States Trade Representative https://ustr.gov/about/policy-offices/press-office/fact-sheets/2026/march/fact-sheet-ustr-initiates-60-section-301-investigations-relating-failures-take-action-forced-labor Accessed: 2026-05-12T08:02:37.087183

[49] USTR Launces Two Section 301 Investigations Focused on Forced Lab https://natlawreview.com/article/ustr-initiates-new-multi-country-section-301-investigations Accessed: 2026-05-12T08:02:37.087183

[50] Tax Insights: USTR initiates new section 301 investigations focused on structural excess capacity and forced labor | PwC Canada https://www.pwc.com/ca/en/services/tax/publications/tax-insights/ustr-new-section-301-investigations-2026.html Accessed: 2026-05-12T08:02:37.087183

[51] Section 301 won’t save Trump’s tariffs if the Supreme Court strikes them down https://thehill.com/opinion/judiciary/5743662-trump-tariffs-section-301/ Accessed: 2026-05-12T08:02:45.470183

[52] CIT Outlines Next Steps for China Section 301 Litigation https://www.kelleydrye.com/viewpoints/blogs/trade-and-manufacturing-monitor/cit-outlines-next-steps-for-china-section-301-litigation Accessed: 2026-05-12T08:02:45.470183

[53] Supreme Court Finds IEEPA Tariffs Unlawful: What You Need to Know | Miller & Chevalier https://www.millerchevalier.com/publication/supreme-court-finds-ieepa-tariffs-unlawful-what-you-need-know Accessed: 2026-05-12T08:02:45.470183

[54] How to Navigate the Section 301 Tariff Process | United States Trade Representative https://www.ustr.gov/issue-areas/enforcement/section-301-investigations/search Accessed: 2026-05-12T08:02:55.414910

[55] Section 301 Tariffs and Retail Supply Chain Uncertainty

https://www.rila.org/blog/2026/05/section-301 Accessed: 2026-05-12T08:02:55.414910

[56] Shapiro | Tariff News | Section 301 Tariffs U.S. Timeline | Chinese Tariffs https://www.shapiro.com/tariffs/tariff-news/ Accessed: 2026-05-12T08:02:55.414910

[57] Section 301 Tariff Lookup: How to Check If Your Product Is on the List - Gaia Dynamics https://www.gaiadynamics.ai/blog/section-301-tariff-how-to-check-if-your-product-is-affected Accessed: 2026-05-12T08:02:55.414910

[58] Your Comprehensive Guide to China's Section 301 Tariffs (2022 Update) https://usacustomsclearance.com/process/section-301-tariffs-a-comprehensive-guide/ Accessed: 2026-05-12T08:02:55.414910

Causal Relationship Graph

Node colors indicate causal confidence rating. Arrows show directional causal relationships identified in this analysis.

Finding Confidence Distribution

Distribution of causal confidence ratings across all findings in this report. CAUSAL findings are fully actionable. MECHANISM findings require additional evidence before action.

This report was published on May 12, 2026. By the time it's free, the market has already moved.

Don't miss the next one.

Don't miss the next one.

This report was published May 12, 2026. Current intelligence reports are available now.